Forecasting and Timing Markets: A Quantitative Approach

- Regular price

-

$39.99 USD - Regular price

-

- Sale price

-

$39.99 USD

Couldn't load pickup availability

Guaranteed Safe Checkout

Description

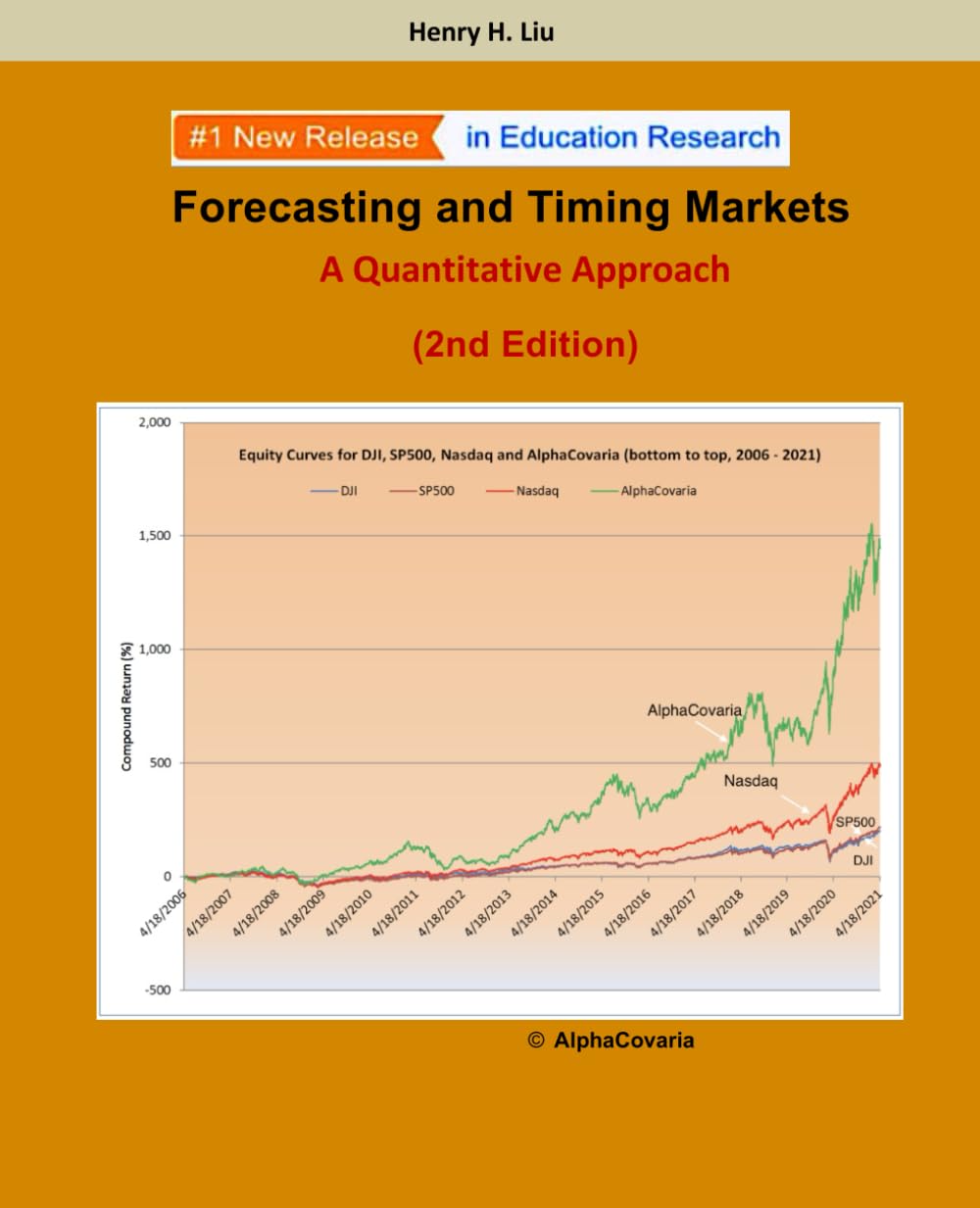

[This is newly published 2nd Edition updated in May 2024, full color version, which demonstrates that 8 out of 9 models beat buy-and-hold (bah) and average Joe's (aj) strategies significantly, based on backtest results with the past 15 years of historical prices.]

Financial markets are essentially time-series data driven events consisting of valleys, peaks, and in-betweens of ups and downs. For more than a century, many pioneers had attempted to come up with various theoretical models to facilitate forecasting and timing market moves. For example, as early as in 1902, or 117 years ago, S. A. Nelson, a friend of Charles H. Dow, attempted to explain Dow’s methods in his book titled The A B C of Stock Speculation, which became later known as “the Dow Theory.” 20 years later in 1922, William Peter Hamilton carried on and wrote the book The Stock Market Barometer, which explained the Dow Theory in more detail. More recently in the last few decades, the advent of advanced computing technologies helped create numerous technical indicators, such as Relative Strength Index (RSI) by J. Welles Wilder (1978), Bollinger Bands (BB) by John Bollinger (2002), Moving Average Convergence Divergence (MACD) by Gerald Appel (2005), Stochastic Oscillator (SO) by George Lane (2007), etc. Those powerful theories and indicators have been heavily studied and well-known in the financial field. However, they are empirical and lack quantitative verifications out of solid backtest results; or they might just be proprietary gauges locked in the computing facilities of those mega financial firms and thus not readily available to the general public.

This text attempts to explore how we can forecast and time markets more quantitatively. For this purpose, the author developed a research-oriented, indicator-based system trading tool, named AlphaCovaria, to help demonstrate how to use various common indicators to forecast and time markets approximately while eliminating subjective speculations at the same time for potentially maximizing profits of trading with a formula-driven approach. The tool consists of three major programs named AlphaCurve, AlphaDriver, and BTDriver, respectively. The AlphaCurve charting tool provides intuitive, all-in-one, specially designed and constructed charts in color to help visualize how various forecasting and timing models work with the price movements of chosen securities and indicators. The AlphaDriver, a data crunching tool, feeds AlphaCurve with market data and computed indicator stats by calling a commercial market data provider. The BTDriveris a backtest driver, which also aggregates profit profiles with a given lookback period, thus enabling the AlphaDriverto generate buy/sell signals on the fly dynamically and adaptively, rather than statically. This work proves that timing markets are achievable if proper indicators, models and strategies are utilized with modern computing technologies.

ASIN: B093B7T7MM

VSKU: GBV.B093B7T7MM.A

Condition: Acceptable

Author/Artist:Liu, Henry H.

Binding: Paperback

Note: Any images shown are stock photographs and product may differ from what is shown.

Condition Notes: This book is in acceptable condition and may have highlighting and or writing throughout. The actual cover image may not match the stock photo, dust jacket may be damaged or missing. Book may show internal and or external wear on spine or cover and may be slightly skewed or have creased pages. This is a used book so codes may be invalid or accompanying media may be missing. May be an Ex library book with stickers and stamps.

ASIN: B093B7T7MM

VSKU: GBV.B093B7T7MM.A

Condition: Acceptable

Author/Artist:Liu, Henry H.

Binding: Paperback

Note: Any images shown are stock photographs and product may differ from what is shown.

Condition Notes: This book is in acceptable condition and may have highlighting and or writing throughout. The actual cover image may not match the stock photo, dust jacket may be damaged or missing. Book may show internal and or external wear on spine or cover and may be slightly skewed or have creased pages. This is a used book so codes may be invalid or accompanying media may be missing. May be an Ex library book with stickers and stamps.

Shipping

- No EU import duties.

- Ships within 1-2 business days.

- Ships in our fully recyclable and biodegradable signature boxes.

Returns

Free Refunds up to 7 days